3QFY11 EPS expected at PKR1.71: KAPCO’s board meeting for announcement of 3QFY11 financial results is scheduled on April 20, 2011. We expect the company to post PAT of PKR1.5bn (EPS: PKR1.71) for 3QFY11 up 50% YoY. 9MFY11 earnings are expected at PKR5.35bn (EPS: PKR6.08).

Escalable component of CPP up 4% YoY: Capacity Purchase Price for 2HFY11 is expected to grow by 3% YoY, led by 4% YoY increase in escalable component amid slight decline in non-escalable component. PKR depreciation by 1.2% and US CPI growth of 0.48% during 1HFY11 shall drive 2HFY11 indexation factor up 1.69% HoH.

O&M cost down 56% YoY; despite 21% QoQ increase: We expect two overhauls to be completed during 3QFY11 which will drive up O&M cost to PKR429mn, up 21% QoQ. However, 3QFY11 O&M cost shall still be 56% lower on YoY basis.

Limited gas availability remains a concern for the company: Monthly generation data for Jan-11 and Feb-11 reveals that there was no gas available to KAPCO during the period with average utilization at 41%. We expect KAPCO to have dispatched 1,263Gwh during 3QFY11, a load factor of 44%.

Spread income to contribute 0.19/share to 3QFY11 EPS: We expect net spread income to add PKR169mn (PKR 0.19/share) to 3QFY11 earnings due to higher reliance on cheaper bank borrowing to fund mounting receivables. Last year, spread income was a negative PKR277mn during 3QFY10 due to high reliance on expensive supplier credit.

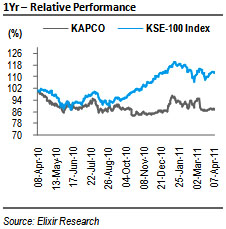

Investment Perspective: With expected final dividend at PKR4.5/share, KAPCO is currently offering dividend yield of 18% for FY11 and real US IRR of 15% over the remaining term of the PPA. At current price levels, KAPCO offers an upside of 26% to our DDM based Dec-11 PT of PKR52/share.

O&M cost down 56% YoY; despite 21% QoQ increase

We expect O&M cost to stand at PKR429mn down 56% YoY. The decline in O&M cost is expected due to base affect as 3QFY10 O&M cost was abnormally high at PKR973mn. We expect two overhauls to be completed during the quarter which will lead to 21% QoQ increase in O&M cost.

Escalable component of CPP up 4% YoY

Capacity Purchase Price (CPP) is expected to grow by 3% YoY for 2HFY11 due to increase in escalable component of CPP by 4% YoY with slight decline in non-escalable component. Growth in escalable component is expected on the back of PKR depreciation of 1.20% and US CPI inflation of 0.48% during 1HFY11 (applicable for 2HFY11 revenues), which shall drive up indexation factor by 1.69% HoH for 2HFY11.

Limited gas availability remains concern for the company

Load factor is expected to remain low for KAPCO during 3QFY11 on the back of low gas availability as LSFO is an expensive generation source. We expect generation for 3Q to stand at 1,263Gwh, which translates into a load factor of 44%. Monthly generation data released by NEPRA for Jan-11 and Feb-11 depicts utilization level of 41% during the first two months of the quarter as well as zero gas supply for KAPCO.

Spread income to contribute 0.19/share to 3QFY11 EPS

We expect other income to stand at PKR2.55bn during 3QFY11, up 1.7x YoY on the back of increase in overdue receivables. We expect net other income (penal markup income less funding cost) for 3QFY11 to stand at PKR169mn (PKR0.19/share), owing to higher reliance on bank borrowing to fund Pepco over dues, which is a cheaper funding source. KAPCO incurred a net loss on funding overdue receivables during 3QFY10 as finance cost was more than penal markup earned on receivables by PKR277mn during the quarter, due to higher dependence on expensive supplier credit.

Investment Perspective

We expect the company to pay final dividend of PKR4.5/share for FY11. The scrip is currently offering dividend yield of 18% for FY11 and real USD IRR of 15% over the remaining life of PPA with WAPDA. Based on our Dec-11 PT of PKR52, KAPCO offers an upside of 26% at current levels.

Economic & Political News

Exports reach new peak

The country exported goods worth USD2.5bn in March, USD727mn more than exports in the corresponding month last year. The country’s imports rose almost 4% to USD3.4bn during the month in review – USD130mn more than the imports posted in the same month last year exports also shrunk the gap between exports and imports by almost 40%. The trade deficit stood at USD920mn, compared with last year’s deficit of USD1.5bn Pakistan’s exports stood at USD17.8bn during the July-March period. Imports during this period stood slightly over USD29bn.

Remittances set USD1bn record in March

The country received USD1.052bn remittances sent by the overseas Pakistani workers in March that was 38% higher than the amount sent during the same month last year

Analyst Certification:

The research analyst(s) denoted AC on the cover of this report, primarily involved in the preparation of this report, certifies that (1) the views expressed in this report accurately reflect his/her personal views about all of the subject companies/securities and (2) no part of his/her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

Disclaimer

The report has been prepared by Elixir Securities Pakistan (Pvt.) Ltd and is for information purpose only. The information and opinions contained herein have been compiled or arrived at based upon information obtained from sources, believed to be reliable and in good faith. Such information has not been independently verified and no guaranty, representation or warranty, expressed or implied is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as, an offer, or solicitation of an offer, to buy or sell any securities or other financial instruments.

Research Dissemination Policy

Elixir Securities Pakistan (Pvt.) Ltd. endeavors to make all reasonable efforts to disseminate research to all eligible clients in a timely manner through either physical or electronic distribution such as mail, fax and/or email. Nevertheless, not all clients may receive the material at the same time.

Company Specific Disclosures

Elixir Securities Pakistan (Pvt.) Ltd. may, to the extent permissible by applicable law or regulation, use the above material, conclusions, research or analysis in which they are based before the material is disseminated to their customers. Elixir Securities Pakistan (Pvt.) Ltd., their respective directors, officers, representatives, employees and/or related persons may have a long or short position in any of the securities or other financial instruments mentioned or issuers described herein at any time and may make a purchase and/or sale, or offer to make a purchase and/or sale of any such securities or other financial instruments from time to time in the open market or otherwise. Elixir Securities Pakistan (Pvt.) Ltd. may make markets in securities or other financial instruments described in this publication, in securities of issuers described herein or in securities underlying or related to such securities. Elixir Securities Pakistan (Pvt.) Ltd. may have recently underwritten the securities of an issuer mentioned herein.

Other Important Disclosures

Foreign currency denominated securities is subject to exchange rate fluctuations which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. Foreign currency denominated securities is subject to exchange rate fluctuations which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk.

![]()

Contributed By

{kind=link}