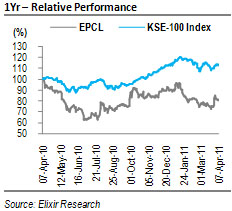

CY11 EPS upped 120%; PT raised: With rising commodity prices, PVC-Ethylene margins have risen significantly. We now expect PVC-Ethylene margins at USD591/ton in CY11 and revise CY11 EPS by 120% to PKR1.17. We have revised our Dec-11 PT by 17% to PKR14/share, indicating a marginal upside of 5% from current levels. The scrip is trading at CY11E P/E multiple of 6x. Hold!

PVC volumes to grow 13% YoY in CY11, margins on the rise: We expect total volumetric sales of PVC (local & exports) to jump 13% YoY in CY11 due to increased availability post commencement of VCM production amid post flood reconstruction activities and healthy demand from pipe segment. In house VCM production will prop up margins by three fold as we estimate PVC-Ethylene margins (USD591/ton as against PVC-Ethylene margins of USD150/ton.

Key risks: Key risk to our valuation and recommendation include 1) Possible disruption in VCM plant operation and resulting need for spot purchases could further weigh down margins and earnings and 2) High financial leverage breeds high earnings sensitivity to margins.

CY11 EPS upped 120%; PT raised!

With recent uptick in commodity prices, international PVC margins have increased significantly, with 1QCY11 PVC-Ethylene margins at USD545/ton (Mar-11: USD582/ton). EPCL’s has also raised domestic PVC prices, with current margins averaging USD582/ton. We now expect PVC-Ethylene margins at USD591/ton in CY11 and revise CY11 EPS by 120% to PKR1.17. The scrip is trading at CY11E P/E multiple of 6x. Hold!

Demand recovery in CY11 along with increased PVC availability

Limited availability of PVC stocks, due to VCM plant disruptions and spot VCM purchases hampered PVC sales during CY10, whereas reduced government spending also hurt PVC demand. While VCM plant has achieved COD, we conservatively expect CY11 PVC production at 120ktons, 80% utilization level. With the likelihood of robust post flood PVC demand, and strong demand of PVC pipes from Afghanistan, we expect 8% YoY surge in local sales of PVC (local & exports) to 105k tons in CY11.The company will need to export a surplus of 15k tons during CY11, where we expect 14% lower retentions as compared to domestic PVC price, leading to 33% lower primary margins on exports as compared to domestic sales.

Healthy margins driving bottom-line green

EPCL had to consume expensive imported VCM due to delays in commencement of the backward integration project. Anticipating timely commencement of VCM plant, the company abolished its long term VCM contract in CY09, which led them to make expensive VCM spot purchases. In house VCM production will prop up margins by three fold as we estimate PVC-Ethylene margins (USD591/ton as against PVC-Ethylene margins of USD150/ton.

Key risks remains VCM plant disruption and sensitivity to interest rates

Possible disruption in VCM plant operation and resulting need for spot purchases could weigh down margins and earnings significantly as integrated PVC-Ethylene margins are 4x of PVC-VCM margins. With PKR13.5bn in debt acquired for expansion/backward integration project, we estimate CY11 financial charges at PKR1.3bn. While higher debts yield a high sensitivity to interest rates, changes in margins could have a leveraged impact on earnings.

Economic & Political News

Reserves slip to USD17.64bn

Pakistan`s foreign exchange reserves eased to USD17.64bn in the week ending on April 2, from a record USD17.95bn the previous week due to schedule debt repayments.

FBR moves to raise PKR572bn in April-June

The Federal Board of Revenue will have to raise PKR572bn in the last quarter of FY11 to reach the downward revised target of PKR1,588bn for the fiscal year. The tax authorities during the first nine months (July-September) of this fiscal year collected a total of PKR1,016bn, registering a 12% increase over the collection made in the corresponding period of last fiscal year.

Analyst Certification:

The research analyst(s) denoted AC on the cover of this report, primarily involved in the preparation of this report, certifies that (1) the views expressed in this report accurately reflect his/her personal views about all of the subject companies/securities and (2) no part of his/her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

Disclaimer

The report has been prepared by Elixir Securities Pakistan (Pvt.) Ltd and is for information purpose only. The information and opinions contained herein have been compiled or arrived at based upon information obtained from sources, believed to be reliable and in good faith. Such information has not been independently verified and no guaranty, representation or warranty, expressed or implied is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as, an offer, or solicitation of an offer, to buy or sell any securities or other financial instruments.

Research Dissemination Policy

Elixir Securities Pakistan (Pvt.) Ltd. endeavors to make all reasonable efforts to disseminate research to all eligible clients in a timely manner through either physical or electronic distribution such as mail, fax and/or email. Nevertheless, not all clients may receive the material at the same time.

Company Specific Disclosures

Elixir Securities Pakistan (Pvt.) Ltd. may, to the extent permissible by applicable law or regulation, use the above material, conclusions, research or analysis in which they are based before the material is disseminated to their customers. Elixir Securities Pakistan (Pvt.) Ltd., their respective directors, officers, representatives, employees and/or related persons may have a long or short position in any of the securities or other financial instruments mentioned or issuers described herein at any time and may make a purchase and/or sale, or offer to make a purchase and/or sale of any such securities or other financial instruments from time to time in the open market or otherwise. Elixir Securities Pakistan (Pvt.) Ltd. may make markets in securities or other financial instruments described in this publication, in securities of issuers described herein or in securities underlying or related to such securities. Elixir Securities Pakistan (Pvt.) Ltd. may have recently underwritten the securities of an issuer mentioned herein.

Other Important Disclosures

Foreign currency denominated securities is subject to exchange rate fluctuations which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. Foreign currency denominated securities is subject to exchange rate fluctuations which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk.

![]()

Contributed By

{kind=link}