Lower than expected 1HCY11 results; but still robust: SHEL posted 1HCY11 earnings at PKR1.4bn (EPS: PKR20.55), up 95% YoY, primarily due to inventory gains. 2QCY11 earnings clocked in at PKR9.47/share, up 104% YoY. In contrast to historical trend, SHEL did not declare interim dividend with 1HCY11 financial results.

GP and inventory gains matched our expectation: SHEL posted gross profit of PKR7.6bn during 1HCY11, largely in line with our expectation of PKR7.5bn. 32% YoY growth in gross profit came on account of inventory gains of PKR2.6bn during 1HCY11.

Opex/GP declined as expected; finance cost increased 70% YoY: Distribution cost during 2QCY11 shrank by 34% owing to 70% YoY lower FO sales. This has caused Opex/GP ratio to decline to 50% during 1HCY11 as against 65% during 1HCY10. With rising receivables from the GoP, SHEL’s finance cost surged by 70% YoY in 2QCY11, leading to 57% YoY jump in finance cost during 1HCY11.

High tax rate at 59.4%: Tax rate during 2QCY11 was 59.4%, partly owing to flood surcharge as barring flood surcharge, tax rate was still high at 51.7%. The increase in tax rate would have been mainly due to deferred tax asset write off, which has recently been a frequent phenomenon for SHEL. 1HCY11 tax rate was recorded at 53.7%.

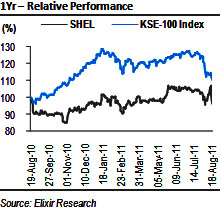

EPS cut on revised estimates: We have revised up our finance cost estimates by 22% for CY11 along with 10% increase in administration cost estimates. In addition, with recent decline in oil prices, we also expect inventory gains would be of much lower quantum during 2HCY11, which would result in lower earnings prospect for SHEL. With the aforementioned changes, we have revised down our CY11 EPS to PKR30.7. At yesterday’s closing price, the scrip offers an upside of 45% to our Jun-12 PT of PKR300/share and offers CY11 dividend yield of 7.3%. BUY!

GP and inventory gains matched our expectations

1HCY11 gross profit met our expectation and clocked in at PKR7.6bn, 32% higher on YoY basis. Growth in GP during 1HCY11 came primarily due to inventory gains of PKR2.6bn, up 90% YoY. 2QCY11 inventory gains estimated at PKR1.4bn resulted in 16% YoY growth in 2Q GP despite 12% YoY lower volumes.

Opex/GP declined as expected; Finance cost increased 70% YoY

Opex/GP ratio declined to 50% during 1HCY11 from 65% in 1HCY10, primarily due to 34% YoY lower distribution cost. Decline in distribution cost was due to 70% YoY plunge in FO sales during 2QCY11 which would have resulted in lower secondary transportation cost. 2QCY11 Opex/GP ratio clocked in at 46%. During 2QCY11 alone SHEL’s receivables from GoP rose by a whopping 117% QoQ to PKR13bn, which has resulted in 70% YoY higher finance cost during the quarter.

High tax rate at 59.4%

Tax rate during the 2QCY11 surged to 59.4%, likely due to flood surcharge and deferred tax asset write off. Barring the flood surcharge tax rate at 51.7% was still high which suggests that SHEL would likely have taken deferred tax asset write off during 2QCY11, which has recently been a frequent phenomenon for SHEL. Excluding flood surcharge, SHEL’s 2QCY11 EPS would likely have been at PKR10.89, while at a normalized 35% tax rate 2QCY11 EPS would have been PKR13.95.

EPS cut on revised estimates

We have revised up our finance cost estimates by 22% for CY11 and administration cost estimates by 10%. In addition, with recent decline in oil prices, we expect inventory gains – which comprised 34% of SHEL’s gross profit during 1HCY11 – would be of much lower quantum during 2H, which would result in lower earnings prospect for SHEL. With the aforementioned changes, we have revised down our CY11 EPS to PKR30.7. At yesterday’s closing price, the scrip offers an upside of 45% to our Jun-12 PT of PKR300/share and offers CY11 dividend yield of 7.3%. BUY!

Economic & Political News

Bid to control circular debt: Power tariff may rise 26% in current fiscal

Consumers are likely to face a 26% increase in electricity rates during the ongoing financial year if government implements power tariff plans A and B to eliminate circular debt and existing subsidy. Under plan A, government plans levying four per cent surcharge on power consumers immediately whereas another 4% surcharge in October, 2% in December and the remaining 4% in February 2012. Under plan B the government plans to recover PKR64bn of this shortfall further increasing the power tariff by 12% and the remaining PKR53.8bn will be subsidized by the government during ongoing financial year 2011-12.

Ministries told to pay PKR25bn to PSO, IPPs by mid-September

Prime Minister Syed Yusuf Raza Gilani has directed the Ministry of Finance and the Ministry Water and Power to pay PKR25bn to PSO and IPPs by mid-September to enable companies to generate electricity to the maximum capacity so that people are subject to minimum load shedding during the Eid holidays.

Analyst Certification:

The research analyst(s) denoted AC on the cover of this report, primarily involved in the preparation of this report, certifies that (1) the views expressed in this report accurately reflect his/her personal views about all of the subject companies/securities and (2) no part of his/her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

Disclaimer

The report has been prepared by Elixir Securities Pakistan (Pvt.) Ltd and is for information purpose only. The information and opinions contained herein have been compiled or arrived at based upon information obtained from sources, believed to be reliable and in good faith. Such information has not been independently verified and no guaranty, representation or warranty, expressed or implied is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as, an offer, or solicitation of an offer, to buy or sell any securities or other financial instruments.

Research Dissemination Policy

Elixir Securities Pakistan (Pvt.) Ltd. endeavors to make all reasonable efforts to disseminate research to all eligible clients in a timely manner through either physical or electronic distribution such as mail, fax and/or email. Nevertheless, not all clients may receive the material at the same time.

Company Specific Disclosures

Elixir Securities Pakistan (Pvt.) Ltd. may, to the extent permissible by applicable law or regulation, use the above material, conclusions, research or analysis in which they are based before the material is disseminated to their customers. Elixir Securities Pakistan (Pvt.) Ltd., their respective directors, officers, representatives, employees and/or related persons may have a long or short position in any of the securities or other financial instruments mentioned or issuers described herein at any time and may make a purchase and/or sale, or offer to make a purchase and/or sale of any such securities or other financial instruments from time to time in the open market or otherwise. Elixir Securities Pakistan (Pvt.) Ltd. may make markets in securities or other financial instruments described in this publication, in securities of issuers described herein or in securities underlying or related to such securities. Elixir Securities Pakistan (Pvt.) Ltd. may have recently underwritten the securities of an issuer mentioned herein.

Other Important Disclosures

Foreign currency denominated securities is subject to exchange rate fluctuations which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk. Foreign currency denominated securities is subject to exchange rate fluctuations which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk.

![]()

Contributed By

{kind=link}